The Real Reason Prices Are Soaring

Andy Snyder|May 3, 2021

There’s a new way to flaunt your wealth in America: Take a trip to the lumber yard.

Back your pickup truck (if you can find one) up to the doors, toss in enough plywood to build a doghouse and drive around town, dropping jaws at every corner.

“I heard it’s old money,” folks will say.

“I heard he’s really down-to-earth,” others will mumble as they ogle the piney gold strewn across your tailgate.

“I bet it’s crypto money,” they’ll say embarrassingly, knowing they too could be holding a fat Home Depot receipt if they had just followed their gut.

No matter… Move over, gold and silver. Lumber has been the commodity of the fortunate over the last 12 months. Its price has more than tripled, boosting the average new home’s construction price – according to at least one estimate – by close to $40,000.

Adding more than $150 per month to the average 30-year mortgage, it’s a price folks will be paying for decades to come.

Ah… the lifestyles of the rich and famous – and their fancy wood-framed homes.

The Story Behind the Story

Certainly you’ve heard about soaring lumber prices.

Just like with the shortage of semiconductors, chicken, gasoline, ketchup, shipping containers and even workers, the media blames the COVID crisis for the problem.

When it comes to wood, the typical news piece says it’s due to an “insufficient domestic supply.”

That’s bunk.

It’s like blaming a poor butterfly for starting Hurricane Andrew by flapping its wings.

The truth is, there’s a lot more at play, and the situation is far more dangerous than the “here today, gone tomorrow” news pieces reveal.

What’s happening across the nation – with almost all of these so-called shortages – is a sign of a much larger problem. It’s a problem we’ve talked about many times in these essays.

It’s the problem of free money.

The truth is that wood production is higher now than it was prior to the COVID crash. It’s at a 13-year high.

The wood is out there.

Go to Home Depot and you’ll see the stuff stacked to the ceiling, like bricks of gold at Fort Knox.

The real issue is demand.

When “Free” Gets Expensive

Here’s the refrain we’ve heard over and over again during recent travels and conversations…

“I didn’t need the stimulus money, but they sent it to me anyway.”

The real issue behind all of these shortages is, of course, government-induced. The near-sighted promise-makers in D.C. saw a temporary problem and “fixed” it with a permanent solution.

To get us through a few months of hard times, they printed trillions of dollars that will ripple through the economy for generations to come. Just ask the fella who will now pay an extra $150 to the mortgage company each month.

He’ll be paying for the free money he got until his retirement.

That $1,200 check will ultimately cost him tens of thousands of dollars.

And the problem isn’t just the stimulus money that most Americans got… but didn’t need.

It’s dirt cheap money too.

Folks are building bigger and fancier homes today because they can borrow money for a price that’s never been lower. Instead of saving a few bucks and building the modest home they would have built if rates were higher, they’re borrowing more cash and adding a couple of extra rooms to their build.

Apparently, the innate human lust for “more and bigger” is not in Jay Powell’s equation.

No Shortage Here…

Yes, lumber prices will fall someday… but not until another crunch forces them to.

In our trading research services, we’re up more than 350% on a play on the lumber industry. The companies behind the boom are seeing record sales amid the soaring demand.

They won’t lower their prices just because new supply is on the market. They’ll lower prices only when demand wanes significantly.

And – thanks to the oodles and oodles of free money – that won’t happen anytime soon.

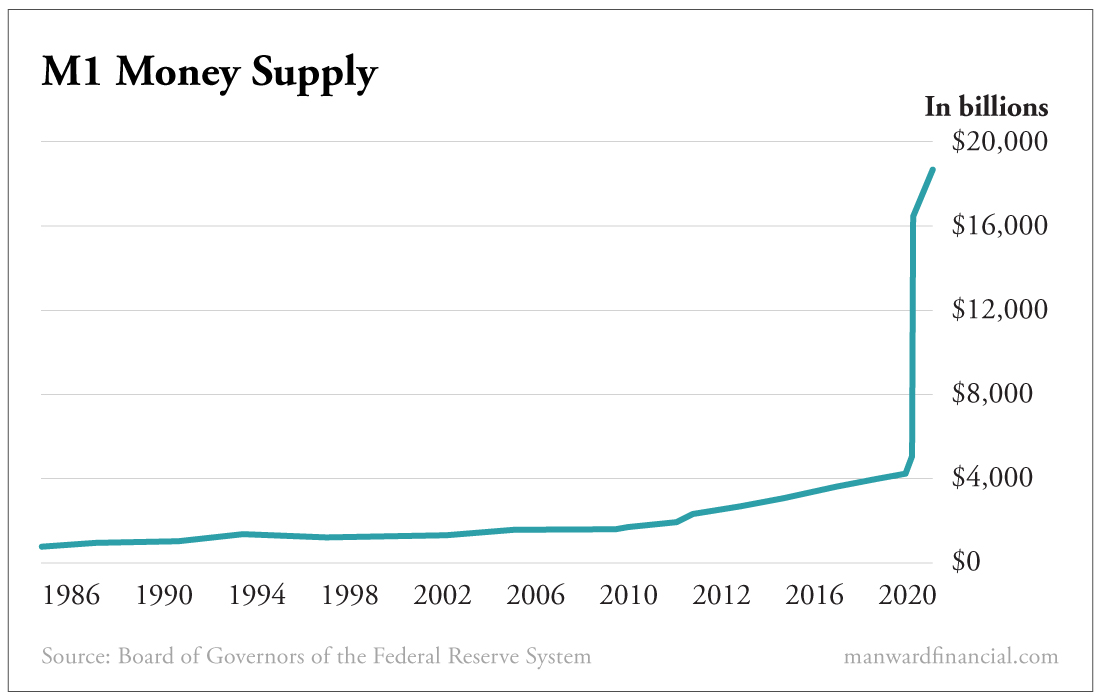

We’ll round third base and head for home by showing you a chart. It’s a chart we showed our subscribers during one of our live Zoom calls.

It shows the M1 money supply. That’s the amount of cash and savings deposits sitting in banks. It’s a measure of the most liquid forms of money.

Hold your jaw before looking at it…

Most folks know that the Federal Reserve printed $4 trillion or so in brand-new money. But few folks understand what that looks like in a fractional reserve banking system… where every new dollar can be sliced and diced into as many as nine more.

Savings and hard currency figures have flat-out boomed, rising by $14 trillion in the last 14 months.

Not only did folks stockpile what they had… but they were also given a whole lot more.

It’s going to take years for the full effects to be felt. Worse yet, we’ll be feeling those effects for many years to come.

It’s time to invest wisely.

Andy Snyder

Andy Snyder is an American author, investor and serial entrepreneur. He cut his teeth at an esteemed financial firm with nearly $100 billion in assets under management. Andy and his ideas have been featured on Fox News, on countless radio stations, and in numerous print and online outlets. He’s been a keynote speaker and panelist at events all over the world, from four-star ballrooms to Capitol hearing rooms.