This Investment Pays More Than Your Job

Andy Snyder|March 21, 2022

Think it’s harder to survive in America today than it was yesterday?

Think it’s harder to make ends meet… or that the “dream” that was promised to you is feeling a bit more like a nightmare?

You’re right. It is.

New figures prove the idea isn’t just a feeling or vague notion. It’s a fact.

The Wall Street Journal published a startling piece last week. The headline says it all: “Homes Earned More for Owners Than Their Jobs Last Year.”

Last year, the value of the average home in the United States surged to $321,634, a jump of $52,667.

Meanwhile, the average full-time worker earned just around $50,000.

It’s great news for folks who own homes. But it’s hell for the 250 million Americans who don’t.

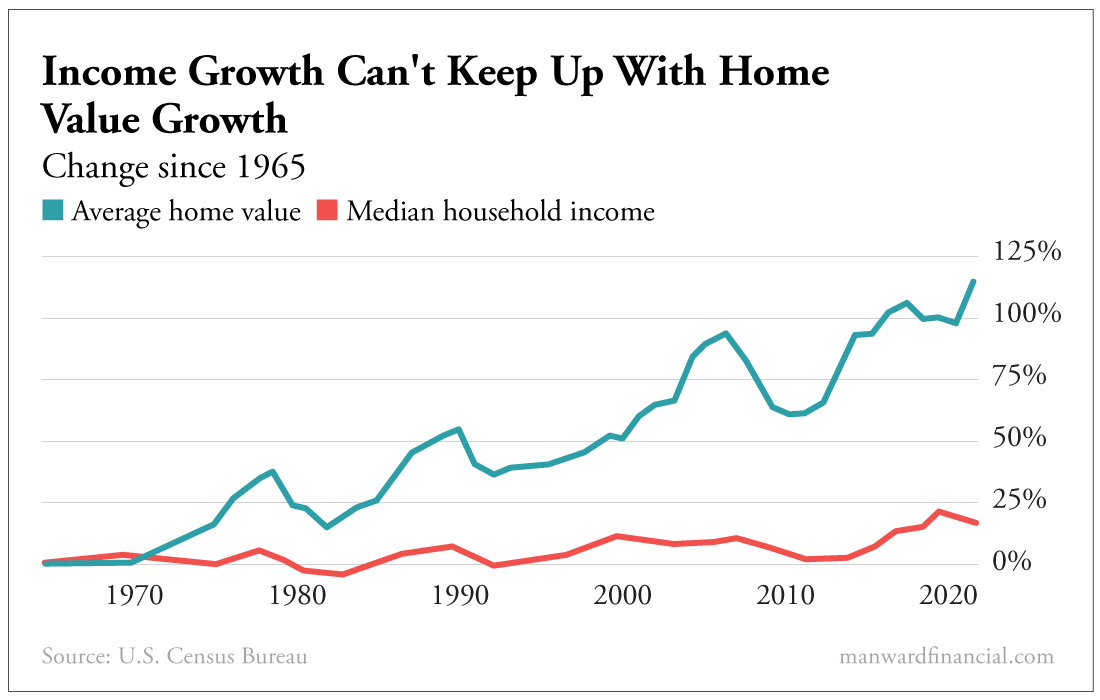

The chart tells the tale…

Keeping the value of the dollar constant (isn’t that a dream?), the nation’s median income has risen 15% since 1965. Meanwhile, the average cost of a home has gone up 118%.

“But Andy,” the keen will say. “Today’s homes are better. They’ve got fancier kitchens, better appliances… They’re more efficient, they have bigger lots… You name it, it’s bigger and better.”

All true.

Comfort levels – much to our nation’s detriment – are at all-time highs.

But tell that to the fella who can’t make rent this month. A smart thermostat doesn’t do much good when you can’t afford the wall it’s screwed to.

Pain

The best way to measure home affordability is by counting how many years of income it takes to buy the average house.

In 1960, for instance, it took 2.1 years of average income to buy the average American home. Today, the figure has surpassed six years.

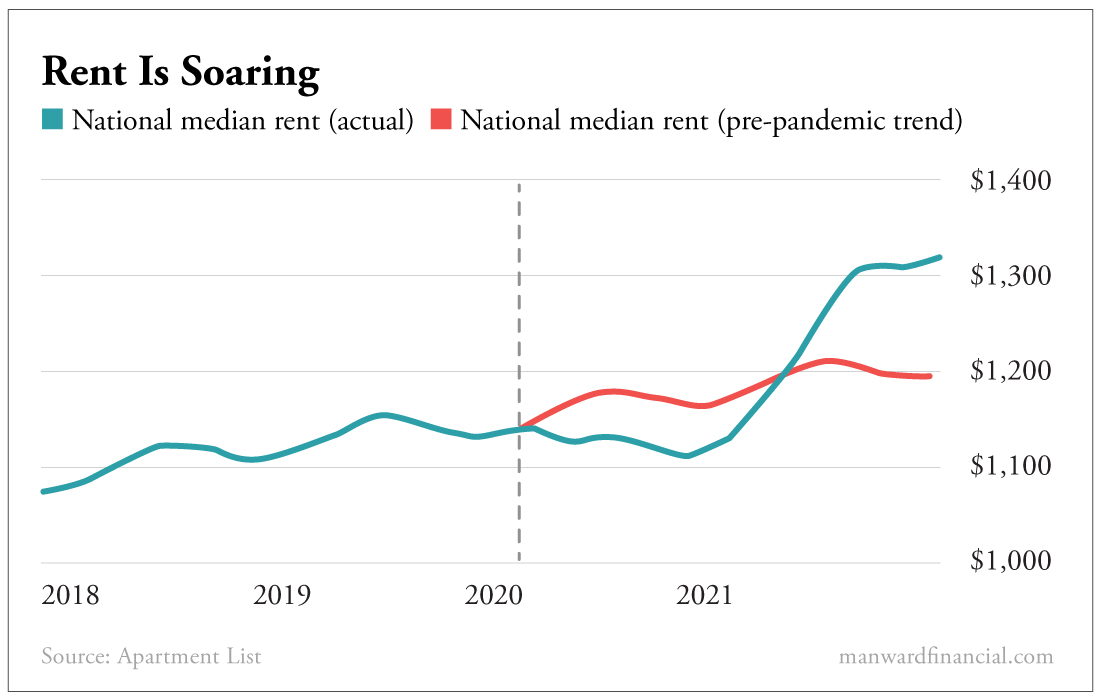

Of course, when homes cost more… landlords want more. That’s a big problem for renters.

The average two-bedroom rental saw its monthly rent surge 22% last year.

But none of this should be news. If you’ve followed our lead, you should be well informed on the subject. We’ve been buying up real estate and writing about our tales for years.

What we should be asking now is what’s causing all of this… and whether it will last.

A Shaky Foundation

There are many supporting reasons prices are surging. Most have to do with bad regulations that needlessly tighten supply or raise the prices of homes.

And we already mentioned another… Homes sell for more these days because they’re worth more.

Like cars that are stuffed with electronics, today’s homes are simply better than homes were decades ago. Therefore, we must pay up… or live in a featureless home that likely doesn’t match today’s overly strict building codes (see bad regulations above).

But there’s a single trend that’s greatly magnified all of these problems.

Bad regulations can’t do their evil if nobody can afford a home. The latest in smart wiring won’t get installed if it’s too expensive. And an entry-level IT worker won’t build a McMansion if he can’t get the loan to pay for it.

In other words, it took something or somebody to fund all of this.

And for that, we look at our fine friends at the Federal Reserve.

Those Dolts

The correlation between low interest rates, money supply and home prices is so obvious that we won’t waste the pixels on a chart.

Like so many economic dysfunctions, this trend got its catalyst on August 15, 1971, the day Nixon removed the nation from the gold standard and made the dollar float on its own lousy merits.

It opened the door for all sorts of shenanigans… like 30-year mortgages that cost a borrower a mere 3%.

Let’s put it this way… The monthly nut on the average American mortgage is $2,033 when rates are at 6.5%. But when the maestros at the Fed wave their wand and pull them down to 3.5%, the figure drops all the way to $1,444.

Your average Joe doesn’t put that $589 in monthly savings into his company-matched 401(k).

No way.

His neighbors won’t drool over his retirement savings. They will, however, drool over his sweet finished basement and home theater.

What a better way to spend life than watching somebody else pretend to enjoy theirs on a big screen on loan from the bank.

But what’s that, Danny, my boy? The pipes are calling? Summer’s gone and all the flowers are dying?

Ah yes, Jay Powell sounded the bagpipes of battle last week. He’s raising rates and putting an end to all this nonsense.

He says he’ll keep prices from rising any further.

We say he doesn’t have the guts.

With the average American now having more than $150,000 in home equity… much of it already leveraged up and spent on other things… Powell and the addicted economy he’s in charge of won’t be able to take the pressure.

They’ll buckle and hand out more free money by the end of the year.

Continue to buy up any good deal you can find.

It’s either that… or wonder how to pay the rent.

Andy Snyder

Andy Snyder is an American author, investor and serial entrepreneur. He cut his teeth at an esteemed financial firm with nearly $100 billion in assets under management. Andy and his ideas have been featured on Fox News, on countless radio stations, and in numerous print and online outlets. He’s been a keynote speaker and panelist at events all over the world, from four-star ballrooms to Capitol hearing rooms.