It’s Not Too Late: Manward’s Guide to Making Dreams Come True

Andy Snyder

Let me tell you a story. It’s a story about money… what most people get wrong about it… and, most importantly, how to make more of it.

It involves an ordinary man named John.

You probably know someone just like him.

John treated himself to a trip to the beach for his 70th birthday. He took a week off from his part-time “retirement” job and rented a house right on the water. He was proud to be able to invite all his children and his grandkids for what he called a “once in a lifetime” event.

“Wouldn’t it be great if we could do this every year,” he said to his daughter as they stared out at the sea.

“We can dream,” she joked. “How about I pay for it when you turn 80?”

“It’s a deal,” John replied, turning to look his daughter in the eye.

Just then, a familiar voice called out.

“Hey neighbor,” called a man from the seaside deck next door. “What brings you to the neighborhood?”

It was John’s old friend from work.

“Oh, hey! We’re here celebrating,” John shouted back. “We’ve got the place for the whole week. How about you? How long are you in town?”

“For as long as the good Lord lets me,” the old friend replied. “We bought the place last year.”

Suddenly, John’s mood soured. He started thinking about his job… his bills… and the future.

He’d be back in 10 years, if he were lucky. His friend never had to go home.

He was jealous of what his friend had created for himself.

It’s easy to see why.

Choices

I’ve talked with a lot of folks about their retirements over the years. When I first entered the world of money management, I was trained to hype the traditional way of reaching financial goals – slow and steady, following the crowd.

But then, after hearing tale after tale like the one above, I changed my tactics.

You see, I found that while the folks in the financial industry tout the compounding nature of money as the greatest force on Earth… there’s something even more powerful.

Its effects compound much faster.

It is, quite simply, our freedom to make choices every day.

One by one, our choices can add up to a life of happiness and abundance… or one of regret and jealousy.

In the story above, John probably made a few small choices that had a dramatic effect on his long-term results.

Maybe he started contributing to a 401(k) a bit late in life. Maybe he bought a bigger house than he needed, expecting a promotion that never came. Or, in an all-too-common scenario, maybe he chose to live in an area with a high cost of living.

Or maybe John being behind his old coworker financially is not his fault. Perhaps a chronic illness put huge medical bills on his plate. Or maybe his children didn’t qualify for big scholarships in school.

The point is it’s rarely one dumb choice that keeps us from our financial goals…

It’s a pile of them that eventually keeps us from rising up.

The good news is that it’s never too late to turn things around.

That’s why I’ve spent the last decade or so speaking to crowds all over the country, teaching ordinary folks how to think, act and invest differently.

Make Fewer Choices

To be fair, when financial experts tout the power of compounding interest, they almost always immediately point to tools that make it harder to make a bad choice.

That’s good.

They point to things like automatic dividend reinvestment. They praise the value of companies that will pay more to shareholders this year than they did last. And they talk about dollar-cost averaging.

All those things mean making the right financial decision is automatic. Aside from switching course, there’s no choice involved.

But lots of folks do those things. Surely there are more folks following these “rules of wealth” than there are truly wealthy people – folks who can, for instance, buy a second home on the water.

So what’s missing?

After two decades in the money business, I’ve narrowed it down to just two things.

The first is a big, fundamentally bad choice – the modern investor’s version of the “original sin.”

It’s that most investors choose to follow an outdated financial model that is, by its very nature, designed to breed mediocrity.

The second, which proves that the consequences of our decisions compound, is that most wealth-seekers never choose to get serious about making money.

If you don’t understand what that last line means, think of it this way…

Very few investors get rich through the traditional “well diversified” portfolio. Sure, they use it as a baseline. But the big money almost always comes from a single powerful investment or strategy.

Warren Buffett purposely used insurance companies to cash flow his empire.

Bill Gates went all-in on getting a computer on every desk.

And Jeff Bezos built a stable financial platform while working on Wall Street and then went after riches by focusing only on creating an online sales platform.

These men aren’t rich because they diversified properly… far from it.

Of course, we can’t all revolutionize the world. But we can use the lessons these titans have taught us to revolutionize our personal wealth.

Spread Wisely

It all starts, of course, with a strong base portfolio. If you’ve ever met with a financial advisor (I used to be one) or read any of the popular financial how-tos, you know the concept.

It’s simple… invest as much as you can afford and spread it across a wide variety of assets. The books tell us a certain amount of our money should be devoted to stocks. A certain amount should go to bonds. Some cash should go toward big companies. Some should go toward younger tech firms.

The logic is straightforward.

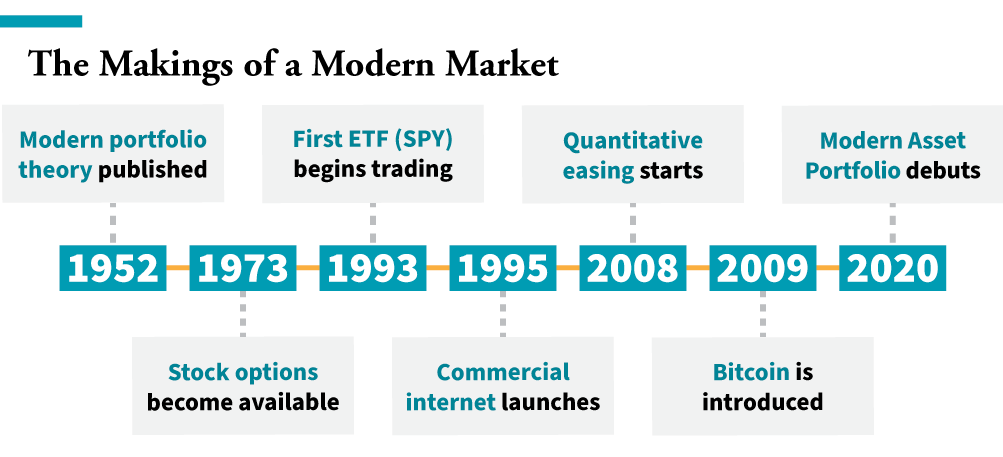

But what most folks don’t know is that this approach to investing was once not all that commonplace. It gained widespread acceptance in the 1950s, shortly after Harry Markowitz wowed the financial world in 1952 with his Nobel Prize-winning “modern portfolio theory.”

In a paper printed in the Journal of Finance simply called “Portfolio Selection,” the father of so-called modern finance showed that an investor can use a mix of correlated and uncorrelated assets to build a portfolio that maximizes returns and minimizes risk.

You’ve surely heard of folks talking about their “set it and forget it” portfolios. They buy a diversified group of assets and walk away, hoping that at any time, at least one of the assets will be doing well.

It’s based on the work of Markowitz. And it’s a sound idea.

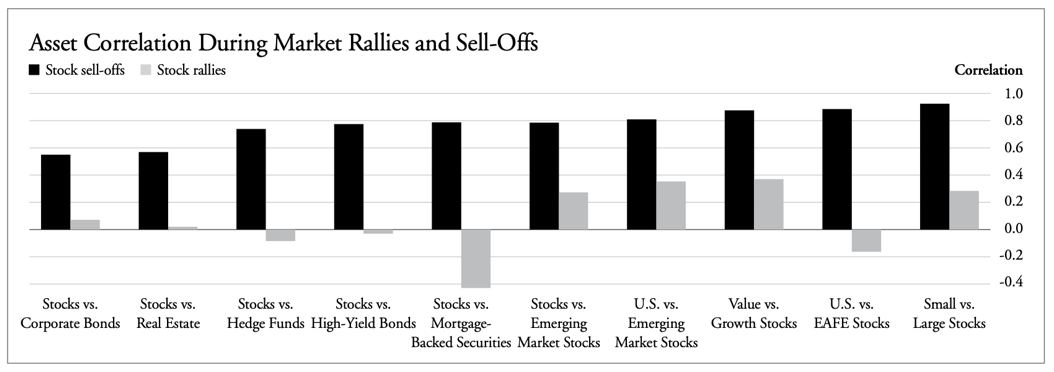

But it’s a recipe for mediocrity. After all, if one asset is doing well, its negatively correlated cousin must be doing poorly.

Two steps forward… one (if you’re lucky) step back.

The problems are multifold.

First, the strategy is far too passive to grow any real wealth. If all Bill Gates had done was work 9 to 5 as a computer engineer and toss a few bucks into his company-matched 401(k) each year, nobody ever would have heard of him.

Over the course of his career – assuming he made every other choice right – he may have been able to retire somewhat comfortably. Not “house on the beach” comfortable… but maybe “rent a place for a few days” comfortable.

And that’s if he got his timing right.

The big problem with Markowitz’s not-so-modern theory (it’s now 70 years old) is that it failed to account for the major financial hiccups that tend to come around every decade or so… when correlations fail and send the whole theory into a tailspin.

Dealing With Trouble

For instance, when the markets crashed in 2008, the correlations that were considered law on Wall Street disappeared overnight.

Everything went down.

The portfolio insurance so many folks had paid for throughout their working lives (in the name of “safe” but moderate returns) failed to pay off exactly when they were needed most.

The same thing happened in 2020. Correlations went bust… and everything lost value.

The dreams of many near-retirees were shattered. The rules they had so diligently followed only held back their returns… The “set it and forget it” portfolio failed to live up to its promise.

And here’s where things get so dangerous… The fix to this problem is obvious.

If our insurance premiums (in this case, in the form of lower annual returns) don’t actually buy us protection, logic tells us to stop paying them.

In other words, we should push the dead weight out of our portfolios.

Lots of folks have done it. They pick and choose which stocks they think will go up the fastest and the furthest.

But like I said, nothing compounds as quickly as the results of our choices.

The folks who got lucky and chose right did very well. They bought the Apples, Amazons and Teslas.

But many more folks didn’t get so lucky. They bought the Enrons, the WorldComs and even the General Electrics.

Again… choices matter. A lot.

Simple Choice

That’s why I created an entirely unique investing model that eliminates one of the riskiest choices investors make. It allows us to stay away from the so-called hedges that do little more than drag our returns down. And it ensures that we’re focused on the stocks that have the very best chances of surging higher… without guessing or gambling.

In a bit of a nod to Markowitz, I dubbed it “modern asset portfolio theory,” or MAP theory.

It’s similar to what Markowitz presented in 1952, but it trades correlations for interest rates – the single most powerful factor in the pricing of modern assets.

Plus, as the name implies, it adds in the moneymaking power of some of the most powerful tools available to investors today… asset classes that did not even exist when Markowitz penned his theory.

It may be hard for younger investors to believe, but the options market – at least the version that we know – has been around only since the 1970s. Exchange-traded funds (ETFs) are far younger. And cryptocurrency, of course, is still an infant.

The bottom line is… things have changed over the last 70 years. Our modern markets look a whole lot different from how they did in the 1950s. That means our investing models should look different too.

And that’s precisely where our MAP theory comes in.

It’s a smarter way to invest. Because with MAP theory, we aren’t focused on how the markets or individual stocks worked more than half a century ago. We’re focused instead on a truly modern market… with an investing model based on what’s happening right now.

Again, we use interest rates to make our investing choices easy. When rates are at one level, we invest a certain way. When they’re at another, we follow the money and invest another way. The whole time, we’re using modern assets to greatly put the odds of success in our favor.

MAP theory has categories aimed at buyback stocks, deflation leaders, blue chips, crypto and a host of others.

It’s a simple solution to what has increasingly become a dangerous model… buying and walking away.

It used to be that “buy and hold” would work. But now… it’s more like “buy and pray.”

Our MAP theory eliminates the problem. It forces us to make smart decisions and not just hope that the strong investments outnumber the weak.

But even as the creator of this revolutionary theory, I know it has its limits. It’s like I wrote above… Few folks have ever funded the life of their dreams with just a diversified portfolio.

If John and his former colleague both had access to the same company 401(k) and the same pay and operated on the same timeline, why is one renting a beach house for a few days… and the other never going home?

It’s because of the choices they made.

Flipping vs. Renting

Most likely, John’s old friend found a way to leverage his success… doubling, tripling or even quadrupling his income potential.

There are lots of ways to get the job done. Some are fast. Some are slow. Some have high risk. Others have very little risk.

Think about the choices folks make when investing in real estate. Some take the slow-and-steady path, buying a home and renting it out for many years. It can work. But owning just one or even two rental units will hardly make you rich… and it certainly won’t do it anytime soon.

That’s why there’s a whole industry devoted to “flipping” houses – buying them when they’re cheap, putting some work into them and selling them for a big profit.

It’s the same general idea… just done quicker and, often, much more profitably.

The best real estate investors do both.

It’s the same situation with stock market investing.

Some folks are in it for long-term gains, while others are trading in and out in a matter of days or, in some cases, minutes.

The trick is not the speed, though. This is critical.

The real value comes back to another choice… how you leverage your wins.

The slow-and-steady crowd takes its profits at the end of the game. For most, it leads to a comfortable yet tight retirement.

The day trading crowd tends to roll its proceeds into the next trade. A $100 trade leads to a $200 trade, which leads to a $400 trade. They’re aiming for a grand slam to end the game.

If all trades were winners, or if we magically knew which trades were losers, the strategy would be an absolute profit machine.

But the stock market hates greed. The folks who never pull money off the table eventually run into a big losing trade that wipes away not only their profits… but also their starting capital.

That’s why I advocate using at least two different short-term trading strategies (at Manward, we focus on two strategies with Codebreaker Profits and Alpha Money Flow)… and that you use the winnings from these strategies to help fund your baseline portfolio.

In other words, if we bank a triple-digit win (turning a $1,000 investment into $2,000) thanks to the volume-screening techniques in Alpha Money Flow, I would not recommend investing $2,000 into our next trade.

Instead… take the $1,000 profit and invest it in the assets recommended in the Modern Asset Portfolio. Add $500 with the next trade… $1,500 with the next… and so on.

Done right, it’s an ideal way to continuously fund a large, rather conservative portfolio that builds real wealth.

It’s like flipping homes to build a portfolio of income-producing rental units. It creates the income you need to build real, lasting wealth.

Before long… you’ll own entire neighborhoods.

Or in the case above… a beautiful house on the beach.

It doesn’t take much to build immense wealth. Compounding wealth is ultimately what makes us rich. But it’s the effects of our compounding choices that ensure we get there.

Make good choices… make great money.

P.S. Take a look at the picture below… It’s proof you can turn your investment profits into the luxuries you’ve always dreamed of having.

P.S. Take a look at the picture below… It’s proof you can turn your investment profits into the luxuries you’ve always dreamed of having.

It’s a picture of the custom boathouse Manward subscriber Vernon G. built using the profits from following our trading research services.

And here’s what he had to say about his subscriptions… “I buy 90% of your recommendations on pure face value. I TRUST your research and methods. I’ve made about $175,000 from your picks.”