When the Recession Will Hit

Robert Ross|August 3, 2023

Everybody wants to be a hero in the markets.

That’s especially true when it comes to calling recessions. As I told you last week, the consensus going into 2023 was that the U.S. would fall into a recession.

Everyone from billionaire investor Ray Dalio and GM CEO Mary Barra to the heads of multiple investment banks expected an economic contraction this year.

But it hasn’t come to fruition.

In fact, the opposite has happened.

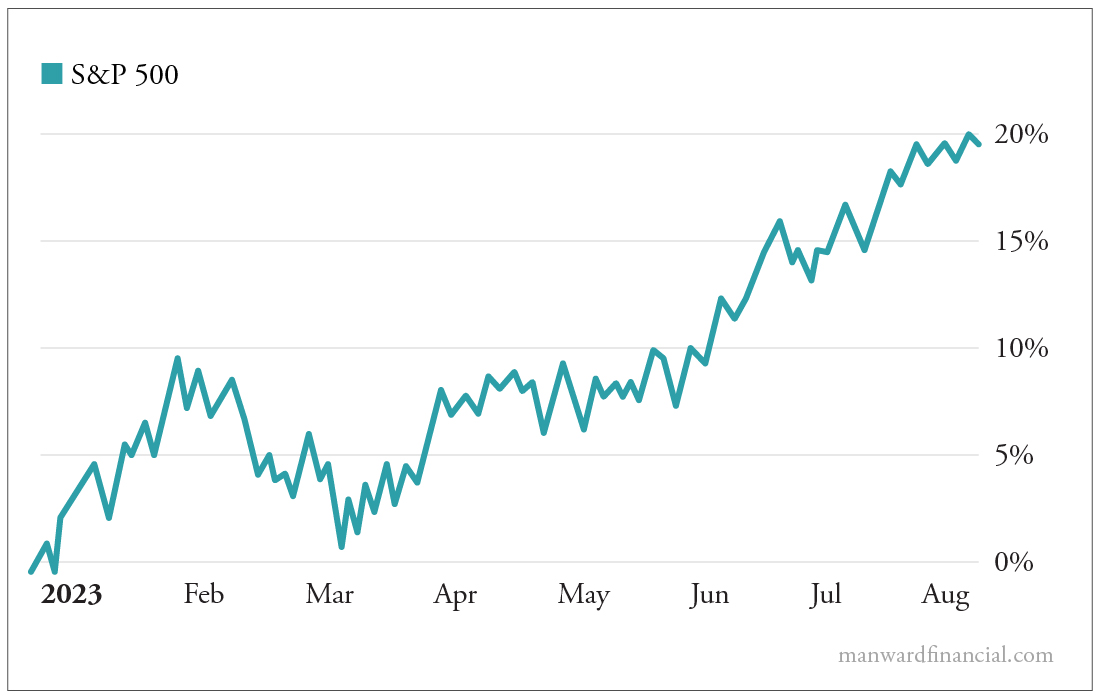

The U.S. economy expanded 2.4% last quarter. The unemployment rate is at a 40-year low. Consumer spending continues to surprise to the upside.

Those are key reasons the S&P 500 is sitting a hair below all-time highs.

Yet many talking heads refuse to throw in the towel… including Peter Schiff, who recently claimed the U.S. is on the brink of the “granddaddy of all recessions.”

These folks are clinging to their recession calls because of something called the yield curve inversion.

But, as I’m about to show you, this indicator – while important – isn’t as useful as you might think.

Upside-Down

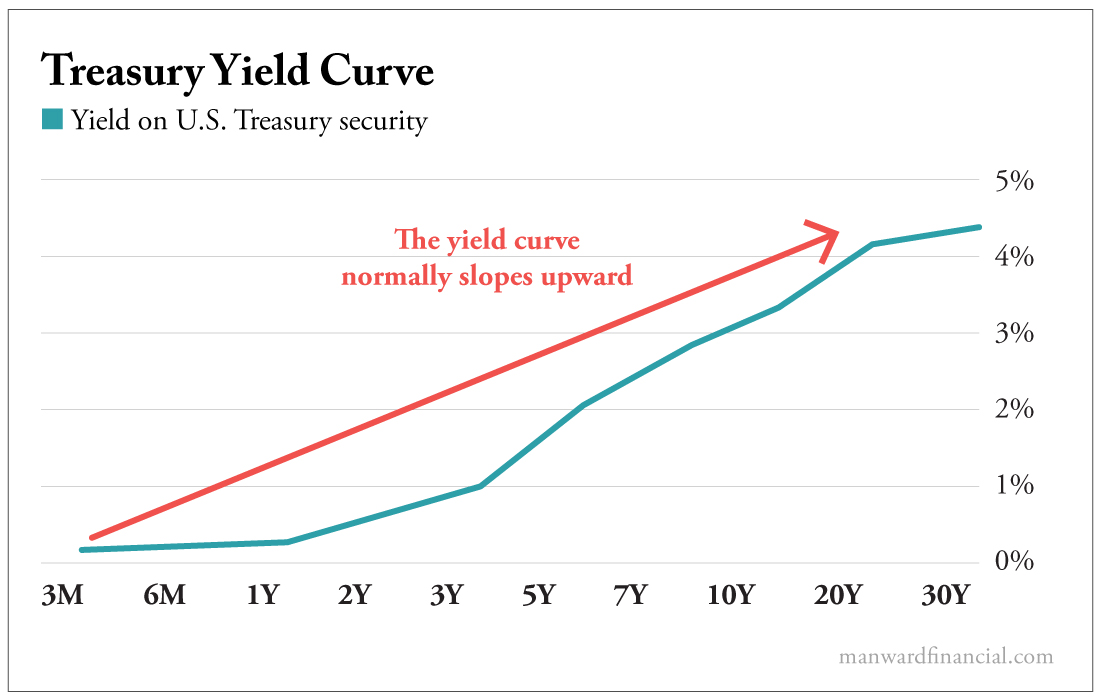

The U.S. government issues bonds to fund its operations.

These bonds are issued for different lengths of time, ranging from three months to 30 years.

Normally, investors demand higher yields from longer-term bonds. This makes sense, as it’s harder to predict economic changes or major world events 30 years out.

In other words, we demand higher yields to compensate for greater uncertainty.

The further out a bond’s maturity is, the higher its yield needs to be.

But when the yield curve inverts, the opposite dynamic plays out. Investors begin demanding higher yields from bonds with shorter time horizons.

That means investors are more nervous about the near term (one to two years) than the long term (10 to 30 years).

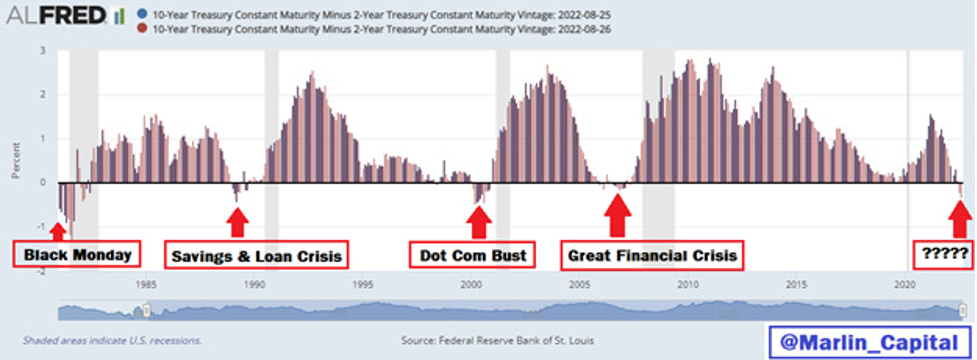

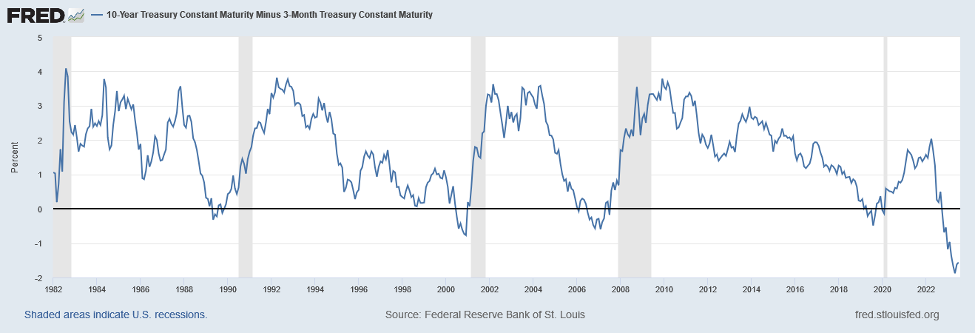

This dynamic has played out before every crisis in the last 60 years.

Clearly, the yield curve inversion has predictive power. And since the curve hasn’t been this inverted in 40 years…

Alarm bells are warranted.

However, while the yield curve is predictive, it is not very useful from an investing standpoint.

Predictive? Yes. Useful? Not Really.

I’m not arguing that the yield curve doesn’t invert before recessions.

Decades of evidence says it does. It’s something I watch to assess the health of the economy.

The issue I have with the yield curve inversion is when analysts use it to make investing decisions.

A yield curve inversion doesn’t tell us when a recession will start, how deep it will go or how long it will last.

As you can imagine, these are important things to know when you’re deciding whether to buy or sell.

For instance, look at this heat map from Fidelity Director of Global Macro Jurrien Timmer:

The red line in the middle shows when each recession started. As you can see, there is a significant and variable lag between when each inversion happened and when each recession hit.

Most economists will tell you that, on average, recessions start 12 to 18 months after the initial yield curve inversion or three to nine months after “peak inversion.” But the lags can be much longer. In fact, they can be so long (e.g., the lags in 1937, 1945, 1949, 1990 and 1994) that many did not even fit on this heat map!

And a yield curve inversion is an even less reliable predictor of when to buy stocks. In fact, on average, the S&P 500 returns 11% in the 12 months after a yield curve inversion hits its deepest point.

Yes, the yield curve has predictive power. But it’s not precise enough to base your investing decisions on.

There Is No Crystal Ball

Every financial talking head wants to call a recession and walk off a hero.

But if you’re interested in making money, worrying about when a recession will hit isn’t helpful.

I know people who went to cash late last year, thinking a brutal recession (and a bear market) was fast approaching. They’ve missed out on huge gains this year.

This is a key reason I advise people to avoid holding a pessimistic market bias. It’s counterproductive.

That’s especially true when the indicators economists use to forecast recessions – like a yield curve inversion – don’t provide actionable information.

Yes, a recession will happen eventually. But don’t try to forecast when it will hit.

Instead, ride the bull market wave as long as it lasts.

Robert Ross

Robert Ross’s unique style of clear and direct stock research helped him build a massive following in the investment research industry, starting his career at investment research company Mauldin Economics and quickly rising through the ranks to become one of the youngest chief analysts in the industry. Today, over a million investors turn to Ross every month for his take on investing, economics, and personal finance. He now shares his unique insights in Total Wealth and Manward Money Report.